For the 2024-2029 mandate, European publishers call on the European Parliament to uphold a vibrant publishing sector, the largest cultural industry in Europe, ensuring that we can continue to freely publish a wide variety of books, guaranteeing freedom of expression, a plurality of opinions and our democratic values.

Search

Members Login

Contact us

European Book Publishing Statistics 2022

8 January 2024

The Federation of European Publishers (FEP) represents 29 national associations of publishers of books, learned journals and educational materials, in all formats, in Europe. The present survey is based on reports from the national book publishing associations, and on further analysis and refining of data, for the year 2022. As of 2019, the survey is based on a new questionnaire, which in the short term will entail limited comparability with some older data and a greater degree of uncertainty regarding some of the figures, but that in the long term will ensure the information is both clearer and more relevant.

Figures on the overall economic significance of the publishing industry refer to net publishers’ turnover, i.e. the publishers’ total revenues from the sales of books, not the total market for books (margin of booksellers or other retailers). They also do not account for revenues in terms of selling rights for translation, audiovisual adaptation, etc. In some cases, only data on market value was available; in such cases, average discount rates were applied to calculate an approximation of net turnover. Figures were rounded conservatively.

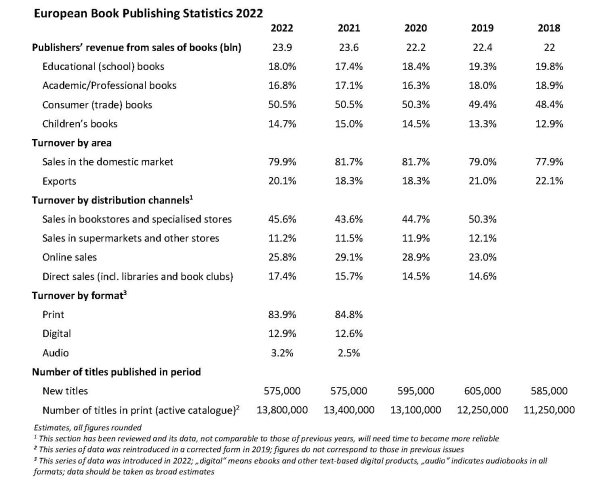

The total annual sales revenue of book publishers of the EU and the EEA in 2022 was approximately € 23.9 billion, according to the survey conducted by FEP. This represents a small increase from 2021 (23.6), the result of mixed outcomes across countries. The largest markets in terms of publishers’ turnover were Germany, the UK, France, Italy and Spain. Total market value is estimated at 36-38 billion €.

A total of about 575,000 new titles were issued by publishers in 2022, about the same as in 2021, possibly due to an attempt at rationalising title production and to competitive pressures. The figure was taken from different sources, some of which included new editions or non-commercial titles, and was rounded conservatively. European publishers held about 13.8 million different titles in stock (some 3.2 million in digital format), the countries reporting the largest availability being the UK, Germany, Italy, France and Spain; this figure has been spiked by the surge in digital publishing (in different formats), the digitisation of back catalogues, the growth of print-on-demand services and the surge in self-published titles, as well as other phenomena. The countries reporting the largest new titles output were the UK, Germany, Spain, Italy and France.

Employment remains an area where it is difficult to gather reliable data. The entire book value chain (including authors, booksellers, printers, designers, etc.) is estimated to employ more than half a million people.

Looking at longer term trends, up to 2007 there was steady growth both in revenues and titles. The 2008 economic crisis had less of an impact on publishing when compared to most other sectors, but revenues still mostly decreased or stagnated until 2014. After 2010, the ebook market grew fast and exports performed well, becoming even stronger from 2015 to 2017. If 2018 marked a trend reversal in the recovery process started in 2015, 2019 confirmed the positive trend. 2020, the year for the pandemic, saw first a very negative impact of the health crisis, but closed with a result only moderately negative, albeit this was the result of many different situations and factors. The pandemic also pushed digital sales up. 2021, while witnessing an impressive – though uneven – recovery, was also the year in which a paper crisis began. In 2022, the market grew overall, but at a much slower pace, with the impact of the paper crisis and geopolitical instability being felt. The ebook market (now around 13% of the total) showed signs of stagnation for the 5 years before Covid (but it could be a matter of capturing the right data), whereas audio book sales exploded in 2019, giving new impetus to digital sales; they passed 3% of the total in 2022.

For further information: Enrico Turrin, +32 2 776 84 64 - eturrin@fep-fee.eu

Pdf version: